Benefits, Eligibility, and How Jet Direct Funding Helps

For New York real estate investors, speed and simplicity often decide who wins the deal. Debt Service Coverage Ratio (DSCR) loans qualify borrowers largely on a property’s cash flow—not on W-2s or tax returns—making them a powerful tool for scaling portfolios across NYC, Long Island, Westchester, the Hudson Valley, and Upstate markets. Below is a practical guide to DSCR loans and how Jet Direct Funding helps New York investors close with confidence.

What Is a DSCR Loan?

This section explains the core concept behind DSCR loans so you can quickly determine if they fit your strategy in New York’s competitive markets.

- Definition: A DSCR loan evaluates whether the property’s income can cover its monthly debt obligations (principal, interest, taxes, insurance, and HOA, if any).

- Focus on the asset: Underwriters place primary emphasis on market rent and/or executed leases instead of your personal tax returns.

- Where used: Common for 1–4 unit rentals and many condos; some programs allow short-term rentals (policy-dependent).

Why New York Investors Choose DSCR Loans

Here’s why DSCR financing is popular from Brooklyn and Queens to Nassau/Suffolk and beyond.

- Qualify on cash flow: Properties with strong rent potential can qualify even when personal income is complex.

- Streamlined documentation: Less emphasis on tax returns can help shorten timelines and reduce friction.

- Portfolio-friendly: Many programs are designed with repeat acquisitions in mind, supporting growth.

- Flexible structures: Options may include LLC vesting, fixed or ARM terms, and payment structures that match your hold strategy.

How DSCR Is Calculated

Understanding the ratio helps you set realistic targets and improve terms before you order an appraisal.

- Formula: DSCR = Property Income ÷ Monthly Debt Service (PITIA).

- Coverage targets: As coverage rises, eligibility and pricing typically improve. Many lenders prefer coverage at or above 1.0x–1.25x.

- What moves the number:

- Income side: Market rent from the appraiser’s rent schedule and/or current leases.

- Expense side: Payment terms, property taxes, insurance, HOA fees, and—where applicable—flood insurance.

Property Types and New York Nuances

Different property types and local rules can impact DSCR outcomes. Plan for these early to avoid surprises.

- 1–4 unit rentals & condos: Widely financed; building budgets, reserves, and rental policies can affect eligibility—especially in NYC.

- Short-term rentals: Some programs allow STRs, but local ordinances, building rules, and documentation standards vary.

- Co-ops: Often ineligible for DSCR programs; when allowed, board rules and subletting restrictions can be limiting.

- Location matters: Coastal areas may require flood coverage; county-by-county tax variations can materially influence PITIA and the DSCR.

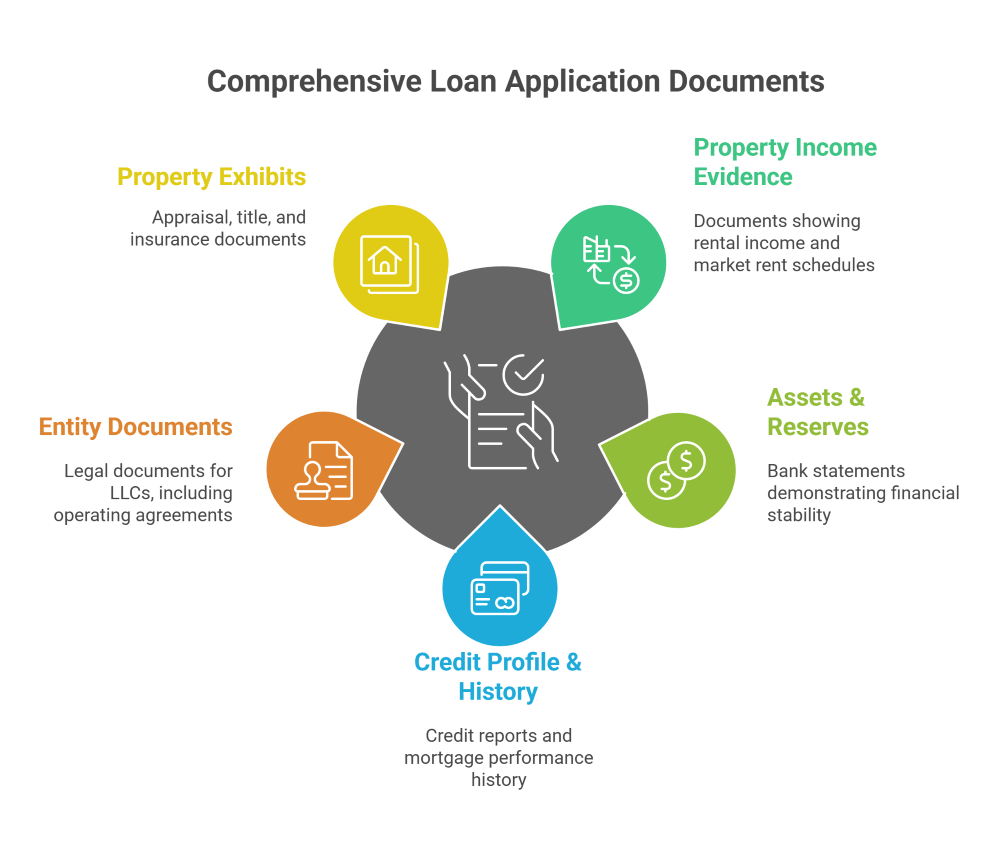

Documentation & Eligibility

While DSCR loans are lighter on personal income paperwork, lenders still verify key components to assess risk.

- Property income evidence: Executed lease(s) and/or the appraiser’s market-rent schedule.

- Assets & reserves: Bank or asset statements to demonstrate closing funds and post-close liquidity.

- Credit profile & housing history: Overall credit behavior and recent mortgage performance.

- Entity documents (if vesting in an LLC): Operating agreement, EIN, and member listing.

- Property exhibits: Appraisal, title, insurance binder, and HOA/condo documents if applicable.

How Jet Direct Funding Helps New York Investors

Think of Jet Direct Funding as your DSCR strategy partner—optimizing structure, timing, and documentation from offer to closing.

- Upfront scenario modeling: We estimate DSCR using current market rents and realistic expense assumptions for New York neighborhoods.

- Local underwriting expertise: We flag building policies, flood zones, and tax/insurance impacts that can shift DSCR and pricing.

- Process management: We coordinate appraisal timing, title, insurance, and entity docs so conditions clear early.

- Options beyond DSCR: If a property narrowly misses the target, we explore alternative structures or timelines to get you to “yes.”

Step-by-Step: The DSCR Loan Process

Use this checklist to keep your file moving and your timeline predictable.

- Discovery & goals: Define neighborhoods, strategy (long-term vs. short-term rentals), and ownership (individual or LLC).

- Pre-analysis: Soft quotes with projected DSCR based on market rent and estimated PITIA.

- Application & disclosures: Credit pull, assets/reserves review, entity documents as needed.

- Appraisal & DSCR confirmation: Appraiser produces market-rent schedule; we finalize structure and terms.

- Underwriting & conditions: Clear insurance, title, HOA/condo documents, and any building approvals.

- Close & plan ahead: Review Closing Disclosure, sign, fund; map next acquisitions using the same playbook.

Who DSCR Loans Fit Best

These borrower profiles often benefit most from DSCR programs in New York.

- Self-employed investors with complex returns or significant write-offs.

- Portfolio builders planning multiple acquisitions across NYC, Long Island, and Upstate.

- Value-add renovators stabilizing rent and optimizing long-term cash flow.

- Buy-and-hold landlords who want scalable, repeatable underwriting focused on the asset.

When to consider other routes:

- Properties with heavy rehab needs better suited to bridge or fix-and-flip financing.

- Buildings or boards with rules that conflict with DSCR program requirements.

- Situations where conventional or agency financing offers a materially better fit.

Practical Tips to Improve Your DSCR Outcome

Small adjustments can meaningfully shift coverage and pricing in New York deals.

- Tight expense estimates: Price taxes, insurance, and HOA accurately; they drive PITIA.

- Lease strategy: Ensure leases reflect market terms and are documented.

- Insurance selection: Verify coverage that satisfies lender requirements without inflating costs.

- Sequence acquisitions: Use DSCR scalability to plan multiple purchases with predictable capital needs.

FAQs

- What DSCR do lenders typically require?

Many programs look for coverage at or above 1.0x–1.25x. Higher coverage generally supports better pricing and terms. - Do I need to provide tax returns?

Typically, no. DSCR emphasizes property income and PITIA. Lenders still evaluate credit, reserves, and housing history. - Can I title in an LLC?

Often yes. You’ll provide your operating agreement, EIN, and member information. - Are short-term rentals eligible in New York?

Some programs permit them, but eligibility depends on local laws and building rules. Verify early. - How fast can I close?

Timelines depend on appraisal scheduling, document readiness, and title clearance. DSCR’s streamlined income review can help. - Are co-ops eligible?

Frequently no, or only under tight conditions. Co-op board policies and subletting restrictions can limit eligibility. - What if my DSCR is just under the target?

We can explore alternative terms, pricing options, or timing adjustments. Re-running scenarios after rent changes or expense updates can help.

Contact Jet Direct Funding

Ready to evaluate your next New York investment with DSCR financing?

- Talk to a DSCR specialist: We’ll model coverage, compare terms, and map a clear path to closing.

- Call or message us today to review your scenario, confirm eligibility, and start your New York DSCR loan application.

Programs, terms, and eligibility are subject to change and underwriting approval.

Key Takeaways

Section intro:

A quick recap for investors who prefer the highlights.

- Asset-based qualification: DSCR loans focus on property cash flow, not your personal tax returns.

- Fit for New York: Works well across NYC boroughs, Long Island, Westchester, and Upstate, with attention to local taxes, insurance, and building rules.

- Speed & scalability: Streamlined documentation and portfolio-friendly structures support growth.

- Plan the details: Accurate rent, tax, insurance, and HOA modeling can meaningfully improve DSCR and pricing.

Partner advantage: Jet Direct Funding guides scenario design, underwrites local nuances, and clears conditions early to keep closings on schedule.

Shachar Rand is Chief Business Development Officer of JDF