Considering an investment property in New York—from NYC condos to Long Island single-families or Upstate multifamily? A Home Equity Line of Credit (HELOC) can offer flexible, on-demand capital to act quickly, renovate strategically, and scale your portfolio. This guide from Jet Direct Funding explains how HELOCs work, where they shine, the risks to manage, and how they compare with other options common to New York investors.

What Is a HELOC?

- A revolving line of credit secured by your home’s equity.

- Draw period (commonly 5–10 years): borrow, repay, and borrow again as needed—often with interest-only minimums.

- Repayment period: line converts to principal + interest payments over a set term.

- Rates are typically variable, so payments can change with market conditions.

New York note: Recording a lien secured by real property generally triggers state and, in some areas, local mortgage recording taxes. Costs vary by county/municipality. Confirm structure and fees early.

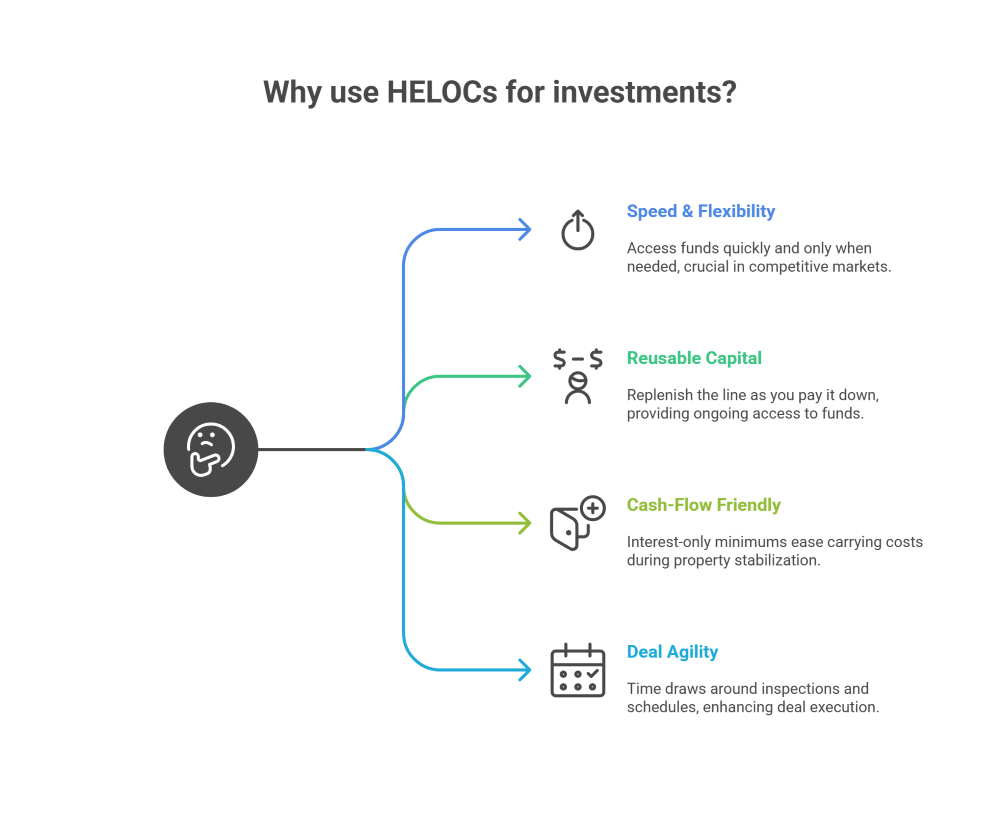

Why New York Investors Use HELOCs

- Speed & flexibility: Access funds quickly and only when needed—useful in competitive New York markets.

- Reusable capital: Replenish the line as you pay it down during the draw period.

- Cash-flow friendly starts: Interest-only minimums during the draw can ease carrying costs while stabilizing a property or completing improvements.

- Deal agility: Ability to time draws around inspections, contractor schedules, or closing timelines.

Key Risks to Weigh

- Variable-rate exposure: Rising rates can increase monthly payments.

- Payment reset: When the draw ends, amortizing payments may be higher—budget ahead.

- Collateral risk: Your primary residence typically secures the line; missed payments can put it at risk.

- Transaction costs in NY: Expect recording taxes and standard third-party fees (appraisal, title, recording).

HELOC vs. Other New York Financing Options (At a Glance)

- Cash-Out Refinance: Replace your existing first mortgage with a larger, usually fixed-rate loan; predictable payments but less flexibility than a revolving line.

- DSCR Investor Loan: The investment property’s cash flow helps drive eligibility; keeps your residence separate from the collateral.

- Home-Equity Loan (Fixed Second): Lump-sum, fixed rate, fully amortizing; more predictable than a HELOC but not revolving.

- Bridge / Fix-and-Flip Loans: Short-term capital for time-sensitive acquisitions and renovations; faster, often at higher rates/fees.

Eligibility & Documentation

- Equity & combined LTV on the property securing the line.

- Credit profile & payment history to gauge pricing and approval.

- Income & DTI (W-2, self-employed, or alternative documentation where applicable).

- Property details for both the collateral home and the target investment (type, occupancy, valuation).

The HELOC Process with Jet Direct Funding (New York)

- Goal setting: Clarify market (NYC, Long Island, Westchester, Upstate), timelines, and funding needs.

- Application & disclosures: Credit pull, income/asset upload, preliminary terms review.

- Appraisal & title: Confirm collateral value and clear title for recording in New York.

- Underwriting & approval: Address conditions early; estimate recording taxes and closing costs.

- Closing & access: Sign, fund, and start the draw period; manage advances as your investment plan unfolds.

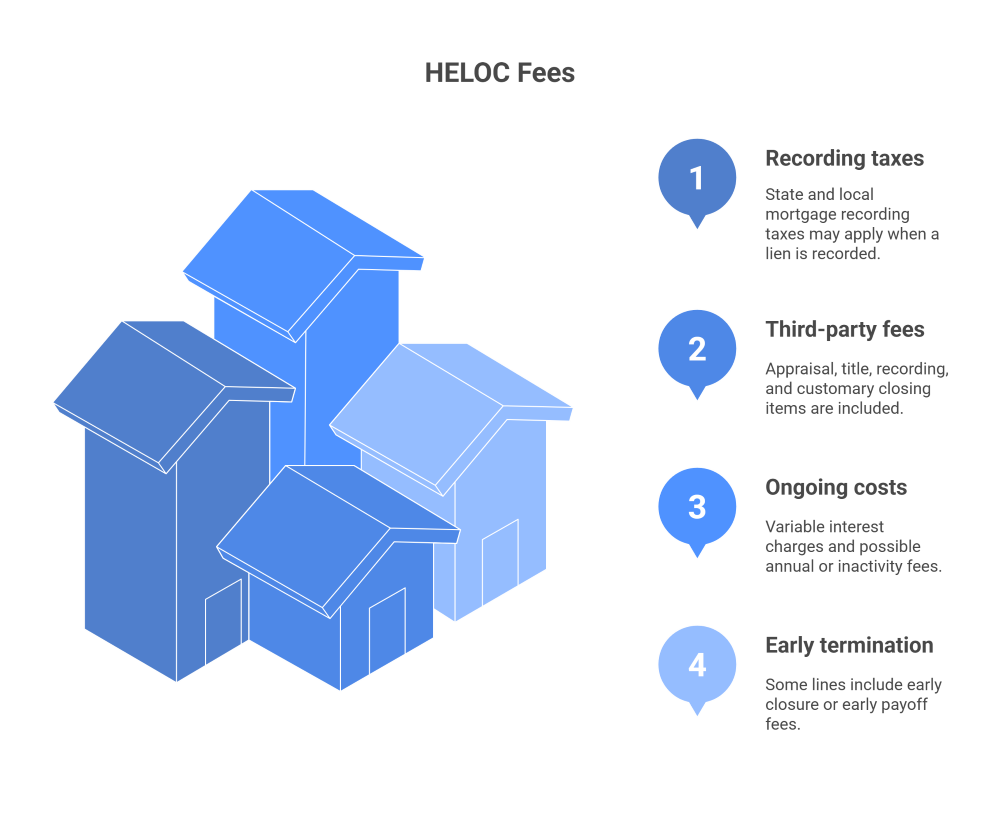

Cost Considerations in New York

- Recording taxes: State (and sometimes city/county) mortgage recording taxes may apply when a lien is recorded.

- Third-party fees: Appraisal, title, recording, and customary closing items.

- Ongoing costs: Variable interest charges; possible annual or inactivity fees per line terms.

- Early termination: Some lines include early closure or early payoff fees—review your agreement.

Practical Tips for Investors

- Stress-test rates: Model payments at higher rate scenarios to protect cash flow.

- Sequence your draws: Time advances to renovation milestones or acquisition events to control interest accrual.

- Keep documentation tight: Track use of funds, contractor invoices, and completion dates—useful for budgeting and future financing.

- Plan the exit: Decide whether you’ll replenish the line via rental income, refinance, or sale.

FAQs

Is HELOC interest tax-deductible if I use the funds for an investment property?

Deductibility is nuanced. Interest on a HELOC is often not treated as home mortgage interest when used for a different property. Depending on use and your tax situation, some or all interest may be treated differently. Consult a qualified tax advisor.

What happens when the draw period ends?

Your line typically converts to amortizing payments of principal and interest, which can be higher than interest-only amounts. Review timing and amounts well in advance.

Can my lender reduce or freeze my HELOC?

Lenders may limit draws under certain conditions (e.g., a significant decline in collateral value or credit changes). Maintaining strong credit and adequate equity helps reduce this risk.

How fast can I close a HELOC in New York?

Timelines vary by appraisal scheduling, title clearance, and documentation speed. Jet Direct Funding moves proactively to keep you on track and communicates milestones throughout.

Will a HELOC affect my ability to qualify for other loans?

Yes. The available line and any drawn balance can impact DTI and reserves. Share your broader financing plan so we can structure accordingly.

Next Step with Jet Direct Funding

If you’re exploring New York investment opportunities and want flexible, on-demand capital, Jet Direct Funding can help you compare a HELOC with alternatives like cash-out refinancing, DSCR loans, and fixed home-equity loans. We’ll model costs, payments, timelines, and risks so you can choose confidently and move quickly.

Key Takeaways

- A HELOC offers flexible, reusable capital for New York investors, with interest-only minimums during the draw and variable rates to monitor.

- Weigh rate risk, payment reset, and collateral exposure against your strategy and timeline.

- Consider alternatives—cash-out refi, DSCR, fixed home-equity, or bridge—based on cost, speed, and predictability.

- Plan ahead for New York recording taxes and standard closing fees.

- Work with Jet Direct Funding to align funding structure with your acquisition and renovation plan, and to map an exit that keeps capital cycling.

Programs, terms, and eligibility are subject to change and underwriting approval. Nothing here is tax, legal, or financial advice. Not a commitment to lend. Equal Housing Lender.

Steven Ho is a seasoned loan officer specialized in NonQM industry with close to 20 years experience.

Grew up in NYC and familiar with the wide array of lending products designed for the underserved community of borrowers.